Determination of the Allocation of Intangible Assets with DEMPE

In conducting affiliated transactions, business entities must of course conduct an in-depth study of the fair price of the transfer for the transaction, this is part of the global regulatory provisions regarding tax avoidance through transfer pricing as well as part of the local provisions in this case the Indonesian tax authorities which are covered by the law. Income Tax and its derivatives.

In the general provisions that the determination of transfer prices between affiliated companies must put forward a principle "If the transaction is made to a non-affiliated party" wherein the general provisions for independent transactions must also be applied to transactions between affiliated companies.

Of all the models and forms of affiliate transactions that often occur and are often carried out by business entities, one of them is the transfer of benefits on Intangible Assets.

Intangible assets are assets that do not have a physical embodiment. Intangible assets have also been referred to as knowledge assets. Most of the focus on intangible assets is on R&D, key personnel, and software. But the notion of intangible assets can be broader to include computerized information (such as software and databases); innovation property (such as scientific and non-scientific R&D, copyright, design, trademark); and economic competence (including Brand Assets, Knowledge Assets of Employees and Experts in the company, aspects of advertising and marketing strategy).

Of course, talking about transfer pricing of intangible assets, there will be many different perspectives (multi-interpretation) between business actors and the tax authorities. It can be understood that the tax authorities are very concerned about this because the imposition of intangible asset allocation costs will cause a decrease in the quality of tax revenues from a country.

There are several strategies that can be taken to avoid tax disputes over the allocation of costs for Intangible Assets, namely in the form of proof of the principle of benefit (benefit substantial affect) and the formation of evidence behind the formation of the Intangible Asset itself.

Further more about and establishing the evidence behind the formation of Intangible Assets in the base erosion and profit shifting (BEPS) initiative initiated by the OECD, developing evidence tools needed by both business actors and tax authorities. determined, one of which is the analysis of the formation of intangible assets. This analysis is based on the mandate of the OECD TP Guideline 2022 in paragraph 6.47 "a determination that a particular group member is the legal owner of intangibles does not, in and of itself, inevitably imply that the legal owner is entitled to any income generated by the business after compensating other members of the MNE group for their contributions in the form of functions performed, assets used, and risks assumed."

The proof of the story behind the formation of Intangible Assets itself is then widely known as "DEMPE" which is a proof of the formation of Intangible Assets based on the allocations of energy and intellectual contributions of various Entities in a Business group on a result of Intangible Assets.

DEMPE stands for DEVELOPMENT - ENHANCEMENT - PROTECTION - EXPLOITATION. Where when formulated in a simple way is as follows:

- By whom and where was the Intangible Asset created/initiated?

- By whom and where is the Intangible Asset strengthened?

- By Who and Where Are Intangible Assets Protected Legally?

- By whom and where the Intangible Asset is exploited.

What is expected is that the imposition of Intangible Asset costs is not always a certainty that the Parent Entity has the right to request an allocation, if carefully weighed, it is possible that the Subsidiary or affiliated parties outside the Parent Entity also have the right to claim the formation of the Intangible Asset.

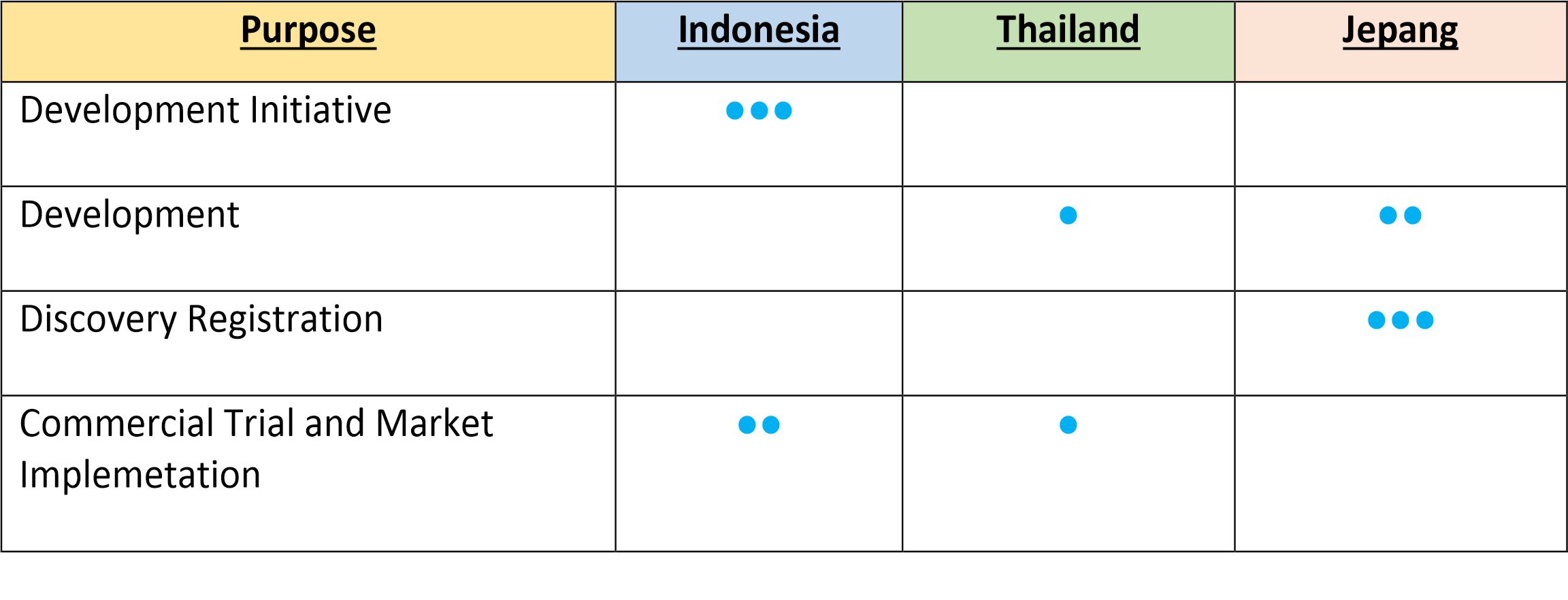

As an illustration of the discovery of a technology which was subsequently discovered by a Parent Entity, namely X, Co.Ltd which is located in Japan, it is billed to all factories that produce -ABCD- products, namely in the form of License Fee which is billed at 2% of sales of -ABCD- products.

From the illustration, it is possible that some tax authorities will go astray and accept the allocation of license fee fees in their authority, because without further investigation, it is possible that manufacturing entities under their authority are only subsidiaries that carry out manufacturing functions that produce -ABCD- products.

If the illustration is analyzed with DEMPE, information is obtained that one technology that was billed by Parent X, Co. Ltd, turns out that the technology was originally initiated in Indonesia, namely in the form of further follow-up claims from customers for the disappointment of the products they purchased on this type. earlier. Then the local analysis team in Indonesia was researched and initiated and then needed the development of the latest technology to cover these shortcomings. Then the parent party, namely X, Co.Ltd ordered the engineer team in Thailand to do further research because the technical facilities in Thailand were quite capable for further development. After this stage the results of research and development are sent to the Parent Company, namely X, Co.Ltd which is then carried out by advanced engineers and facilities in Japan, refinements and final improvements are made which in the end a perfect technological formulation is obtained and patented in Japan. . From one finding, the technology was implemented for the first time on production at factories in Indonesia and Thailand, this is reasonable because in addition to the absorption of the Indonesian and Thai markets for the highest product -ABCD- in the world, the first time complaints were obtained from customers also occurred in Indonesia. After the successful implementation of the technology, production with this technology is then carried out throughout the world where the company has a production plant.

So, based on the illustration, it should be stated in the DEMPE table that Indonesia and Thailand have contributed to the formation of the technology and naturally if there is a claim from tax authorities outside Japan on tax receipts from license fees.

With this simple table, a temporary conclusion can be drawn that there is a territorial contribution from Indonesia and Thailand to the formation of this technology, and this is what all parties want that the transparency of the allocation of the License Fee must be fair and transparent so that the Tax Authorities in Indonesia and Thailand can may request an "allocation allotment" for the License Fee bill. However, in practice, the contribution allocation of the DEMPE function must be assessed very accurately based on accurate data and evidence so that the DEMPE allocation table has a clear level of contribution to value creation. Before the distribution of returns is estimated, it is necessary to assess the level of contribution of the different functions to the value creation process.

For this reason, IKRA Consulting can assist business actors in identifying and allocating the DEMPE function, which in this case is very useful in arguing in tax disputes and in conducting initial explanations to tax authorities.